Infographics: Cost of Living vs. Cost of Borrowing

Here is the graph illustrating the trends in U.S. credit card debt from 2008 to 2024. It shows the initial rise during the financial crisis, subsequent decline during recovery, and a sharp increase in recent years, reaching record highs.

The graph compares the growth in food, rent, and energy costs to wage increases over the past 20 years (2004–2024). It clearly shows that while wages have risen modestly, the costs of essential living expenses have outpaced them significantly, putting pressure on household budgets.

This graph highlights the relationship between vehicle leasing costs and credit score rankings over the last 10 years. It illustrates the following key trends:

This graph illustrates the average monthly leasing costs for homes/apartments over the past 10 years, categorized by credit score rankings:

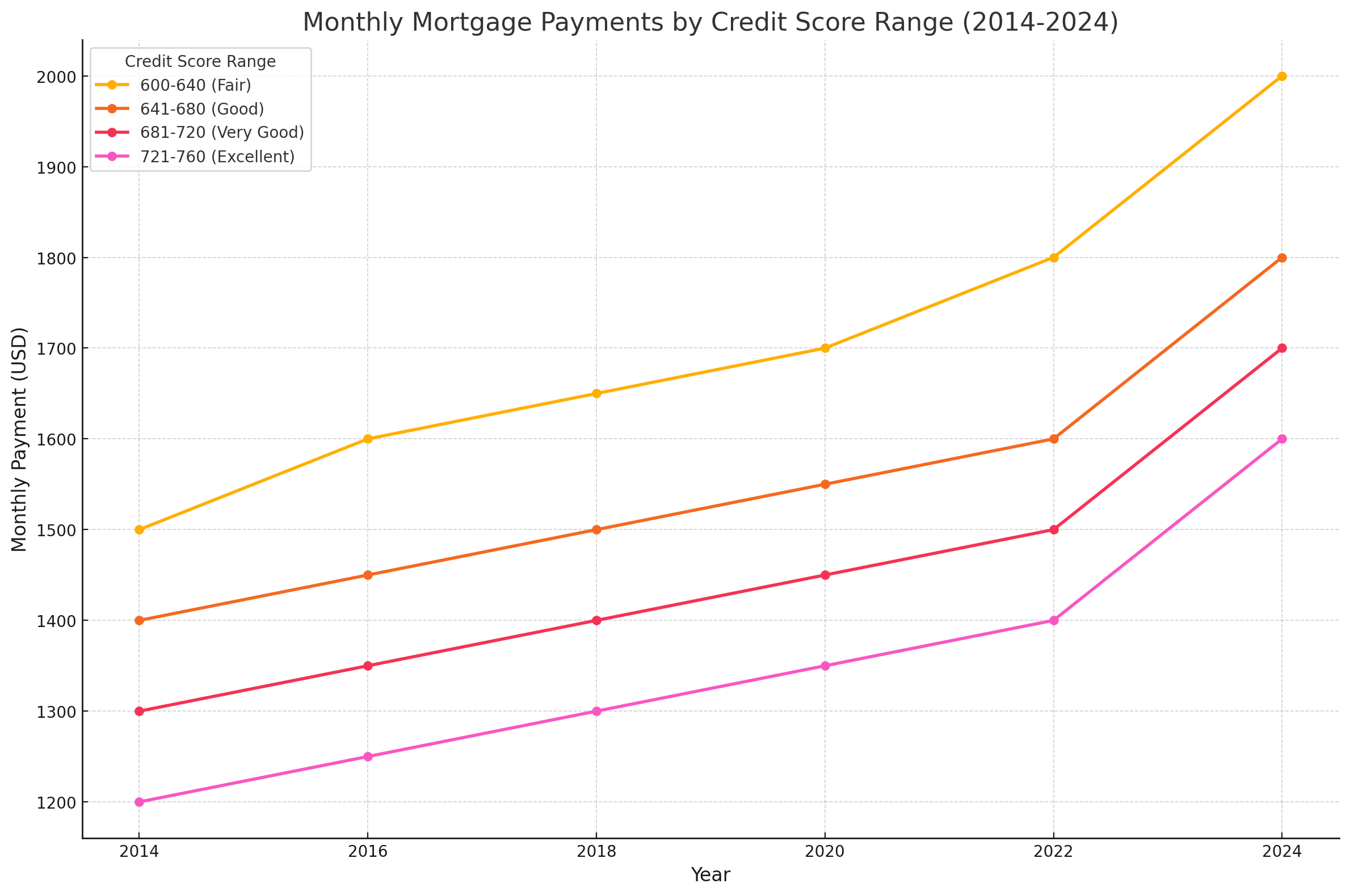

The graph illustrates the monthly mortgage payments for different credit score ranges over the last 10 years (2014–2024). Key insights include:

This graph illustrates the monthly payment costs for a $30,000 HELOC over the last 10 years based on credit score tiers. It highlights the significant difference in costs between borrowers with fair credit (600-640) and those with excellent credit (750+).

APR Trends for Unsecured Loans (2014-2024):

The graph illustrates the average monthly payments for a $20,000 unsecured loan over the last 10 years, segmented by credit score categories:

This graph highlights the average monthly payment for a $40,000 unsecured loan over the past 10 years, broken down by credit score ranges:

This graph highlights the average monthly payment for a $60,000 unsecured loan over a 10-year term based on credit score categories from 2014 to 2024. Key insights include:

The graph shows average monthly payments for an $80,000 unsecured loan (5-year term) by credit score (Excellent to Poor) from 2014-2024, highlighting the impact of credit scores on borrowing costs.

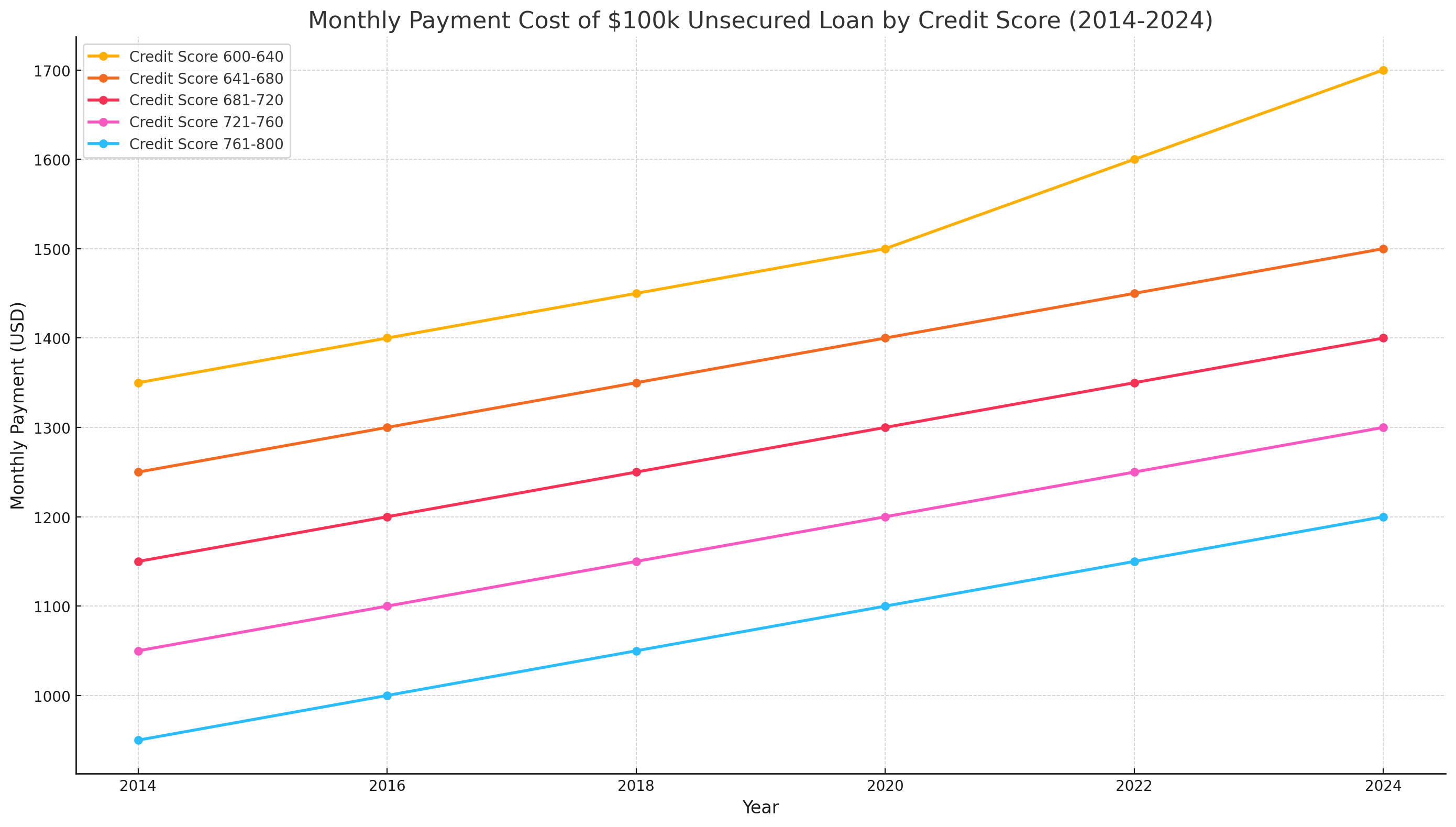

This graph highlights the monthly payment costs for a $100,000 unsecured loan over the last 10 years, segmented by credit score ranges. It demonstrates how credit score directly affects loan repayment amounts, with lower scores incurring higher monthly payments due to higher interest rates.

This graph highlights the monthly payment costs for a $150,000 unsecured loan over the last 10 years, segmented by credit score ranges. It demonstrates how credit score directly affects loan repayment amounts, with lower scores incurring higher monthly payments due to higher interest rates.

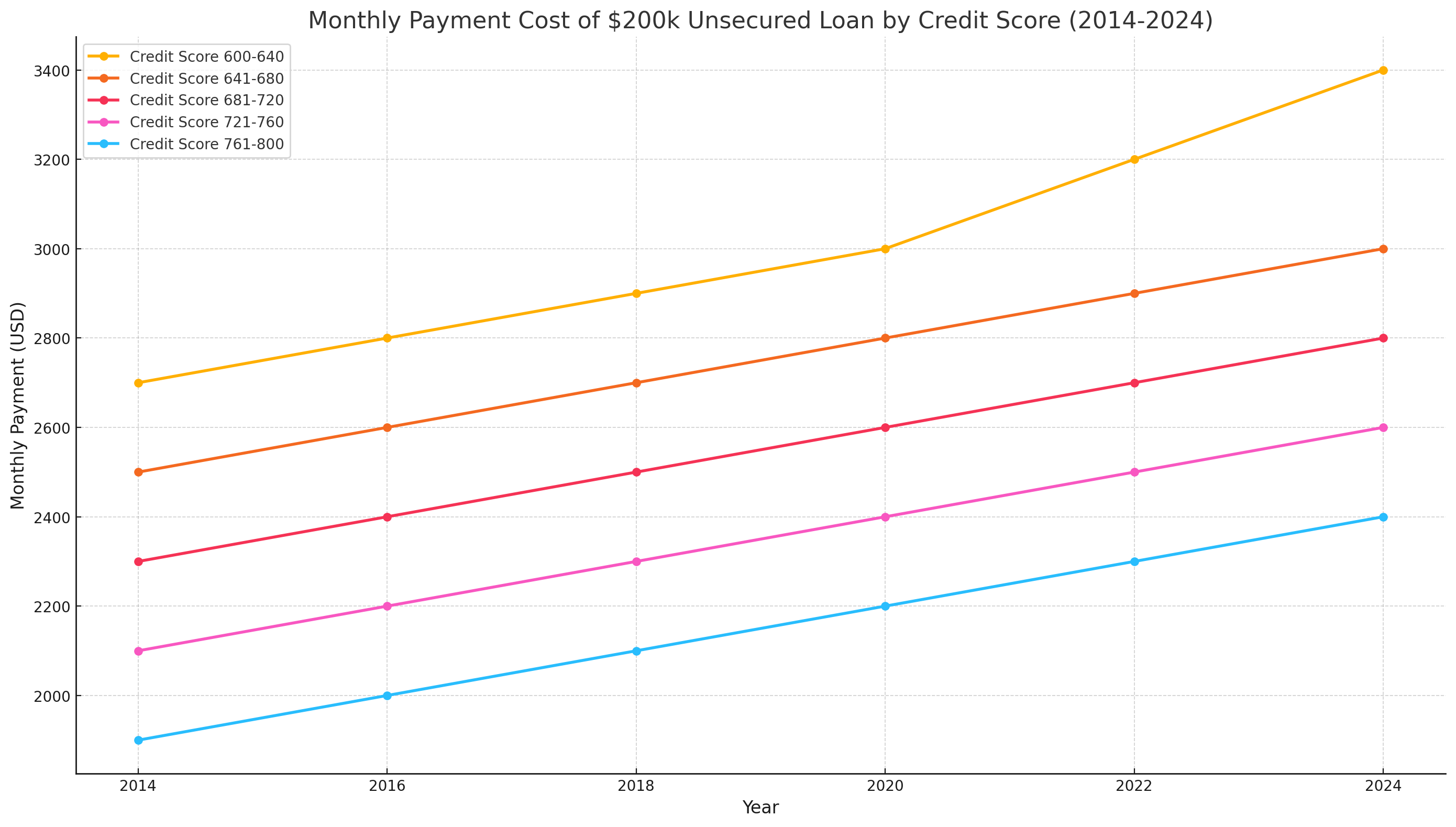

This graph highlights the monthly payment costs for a $200,000 unsecured loan over the last 10 years, segmented by credit score ranges. It demonstrates how credit score directly affects loan repayment amounts, with lower scores incurring higher monthly payments due to higher interest rates.

Here's a graph comparing the average credit score recovery times for different debt relief methods. Debt settlement typically shows faster recovery than bankruptcy and credit counseling. Unsecured loans with high-interest rates have a lengthy recovery timeline.

How Debt Settlement Can Relieve Stress and Strengthen Your Financial Future

Boost Your Monthly Cash Flow Debt settlement can help you take control by reducing or eliminating high-interest credit card debt. This frees up a significant portion of your income, giving you the financial breathing room to cover essentials like food, rent, and energy costs—especially critical as living expenses continue to rise faster than wages.

Ease Financial Anxiety Living with debt can be overwhelming, both emotionally and mentally, especially when paired with increasing economic pressures. Debt settlement offers a clear, actionable solution to lighten your financial burden, allowing you to focus on what truly matters in your life with less stress and worry.

Break Free from the Debt Cycle High-interest rates can create a frustrating cycle, where minimum payments barely make a dent, and debt continues to grow. By addressing the root of the problem, settlement provides an opportunity to reset and move forward on a more stable financial footing.

Focus on What Matters Most With reduced monthly debt obligations, you can redirect your money and energy toward building savings, managing unexpected expenses, or investing in your priorities—whether it’s healthcare, education, or planning for your future.

Debt settlement is more than just a financial strategy; it’s a chance to regain control, simplify your finances, and build a stronger, more secure future for yourself and your loved ones. You have the power to take this step, and we're here to support you every step of the way.